Planning and Cost Risks in Renewable Mega‑Projects

Western Australia (WA) is experiencing one of the largest renewable‑energy investment surges in the world. A record volume of wind, solar, hydrogen and critical‑minerals proposals is now in the State’s approvals pipeline, prompting the government to establish a dedicated Green Energy Major Projects unit to streamline assessment pathways. The scale of this pipeline is unprecedented: multi‑gigawatt hubs, hybrid generation precincts and hydrogen‑export platforms are moving into planning phases. Recent announcements include the Western Green Energy Hub, sized at an extraordinary 70 GW of wind and solar—equivalent to Australia’s entire NEM capacity—targeted at green hydrogen and e‑fuels production.

But WA’s geography shapes both opportunity and risk. Renewable mega‑projects are typically located in remote regions (the Goldfields, Pilbara, Gascoyne and south‑eastern coastal tablelands) where infrastructure is sparse, distances are vast and cost drivers behave differently than in metropolitan contexts. Analysis of major proposals shows that logistics, transmission access, labour availability and inflation exposure often outweigh the cost of turbines, panels or electrolysers. For developers, the critical challenge is designing delivery models, phasing strategies and governance frameworks that can absorb, mitigate or transfer these uniquely regional risks.

Market Context

The Western Australian Government has acknowledged the sheer volume of green‑energy proposals under environmental assessment and has established a cross‑agency initiative to support proponents and investors navigating approvals. The State’s broader 2025–26 policy environment reinforces this momentum: the WA Budget includes more than $584 million for transmission upgrades under Western Power’s Clean Energy Link North, intended to unlock new renewable generation capacity.

At the same time, global‑scale mega‑projects—such as the Western Green Energy Hub and the AREH in the Pilbara—demonstrate intense international interest in WA as a hydrogen and e‑fuels export base. These proposals rely on remote coastal access, high‑quality wind and solar resource bands, and proximity to export infrastructure.

For developers, this context translates into:

High competition for land and approvals in strategic areas.

Growing pressure on transmission corridors to accommodate new load and generation.

Escalating labour competition, particularly in construction and renewable operations.

Sensitivity to global inflation in materials, shipping and EPC contracts.

Commercial and Cost Implications

Land and approvals risk

WA’s environmental approvals framework is evolving to manage renewable mega‑project demand. While the Green Energy Approvals Initiative seeks to shorten assessment timeframes, proponents face:

complex biodiversity baselines,

native‑title negotiations, and

overlapping State and Commonwealth referral triggers.

These conditions matter because delays directly increase preliminaries, financing costs and inflation exposure. Mega‑projects like WGEH have multi‑stage approvals spanning thousands of square kilometres, demonstrating how permitting becomes a long‑duration cost driver.

Transmission and grid access

Transmission scarcity is a defining constraint. WA’s 2025–26 Budget allocates over $584 million for network investment to unlock new renewable zones, but long‑distance transmission remains capital‑intensive and environmentally sensitive. Remote projects often require:

hundreds of kilometres of new transmission,

substation construction in non‑metropolitan regions, and

coordination with mining‑sector loads competing for capacity.

For hydrogen projects, grid constraints also drive decisions on behind‑the‑meter generation and hybrid system sizing. Transmission uncertainty is one of the largest determinants of staging risk.

Logistics & labour (dominant cost risks)

Remote conditions make logistics the single most material cost risk for WA mega‑projects. Developers must consider:

long‑distance transport of heavy components across desert regions,

limited port capacity for outsized wind‑turbine equipment,

local road upgrades for abnormal loads, and

fly‑in/fly‑out (FIFO) labour competing with mining.

Large projects such as WGEH illustrate these constraints: despite world‑class resource bands, the region is near‑deserted, requiring multi‑stage infrastructure development for access, water and hydrogen processing. Labour scarcity also amplifies escalation risk given WA’s mining sector continues to bid up skilled resource wages.

Inflation sensitivity

Mega‑projects with delivery windows spanning 10–30 years are highly exposed to:

global EPC inflation,

volatility in steel and electrical equipment, and

high‑voltage equipment lead times.

Renewable hydrogen projects add further complexity: electrolyser costs are linked to global manufacturing cycles and shipping bottlenecks. Inflationary volatility can compound significantly where approvals or transmission access are delayed.

Phasing strategy

Multi‑gigawatt projects, such as WGEH’s 30‑year staged build‑out, benefit from:

modular staging of wind and solar arrays,

early works packages to de‑risk access and logistics,

flexible procurement windows to hedge inflation, and

phased hydrogen/ammonia processing aligned to market depth.

Phasing also allows cost learning across packages, reducing exposure to early‑stage estimates.

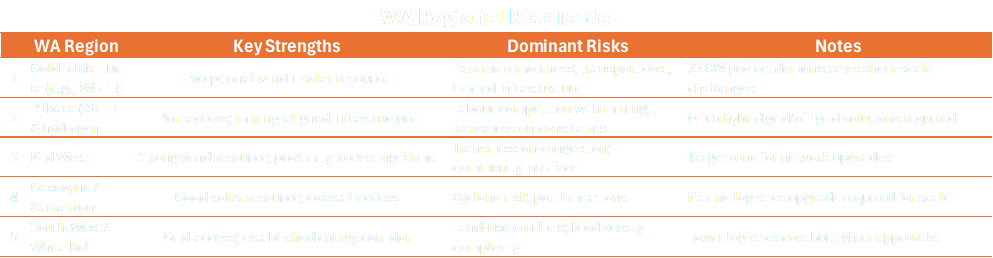

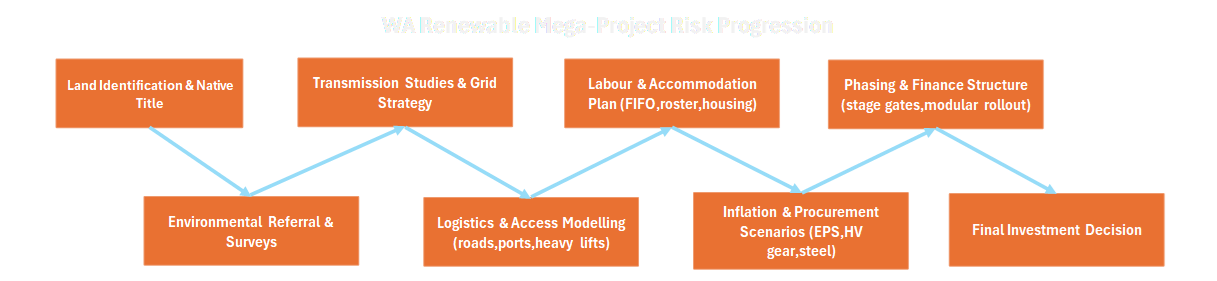

Synthesising risks across major WA renewable regions. Sources include WA Government approvals insights and published mega‑project contexts.

Shows how early‑stage decisions compound downstream cost exposure

Sources: WA Government major project guidance; renewable mega‑project case details.

Practical Takeaways

Remote‑location logistics dominate cost risk; factor early‑stage access, heavy‑haul constraints and labour mobility into feasibility assumptions.

Transmission access remains the biggest planning determinant; uncertainty inflates contingency and can distort phasing.

Approvals sequencing is critical: biodiversity constraints, native title and water access shape schedule more than technology choices.

Inflation modelling must be dynamic, particularly for long‑lead equipment (HV gear, electrolysers, structural steel).

Staged delivery unlocks cost learning, mitigates inflation exposure and smooths labour demand.

How QIA Can Assist

Quantum Insights Advisory supports renewable developers in feasibility cost planning, with a focus on remote‑region logistics, access constraints and staged delivery pathways. We use risk‑based contingency modelling to quantify transmission uncertainty, escalation risk and procurement volatility across multi‑gigawatt project horizons. Our commercial controls frameworks establish clear governance around approvals sequencing, contracting strategy, data discipline and performance tracking. Where carbon considerations affect design—such as embodied emissions or renewable‑powered construction—we integrate carbon management into cost and phasing analysis. For proponents navigating complex land, native‑title or logistical interfaces, QIA provides expert advisory on risk allocation, audit‑ready documentation and schedule evidence that supports financing and due diligence. We focus on structured, defensible decision‑making that aligns developer strategy with WA’s rapidly evolving renewable‑energy landscape.

References

WA Government — Green Energy Major Projects approvals and pipeline data. [wa.gov.au]

WALGA — Renewable Energy in WA research (regional transition context). [walga.asn.au]

RenewEconomy — Western Green Energy Hub 70 GW approvals announcement. [reneweconomy.com.au]

Discovery Alert — WA energy transition policy and investment strategy. [discoverya...ert.com.au]

Climate Corporate — WA’s 2025–26 transmission and energy‑transition Budget. [climatecorporate.com]

Austrade — Western Green Energy Hub hydrogen/e‑fuels project profile. [internatio...ade.gov.au]